Penalty for not late filing deadlines for 2026-27

Missing the regular filing timelines for AY 2026-27 subjects you to a mandatory late fee under Section 234F of ₹5,000 if your total income exceeds ₹5 lakh, or a capped fee of ₹1,000 if your income is ₹5 lakh or less. Additionally, you will face an interest penalty of 1% per month under Section 234A on any unpaid tax, forfeit the right to carry forward financial losses, and lose the choice to opt for the Old Tax Regime.

5/22/202610 min read

Filing your Income Tax Return (ITR) is a critical annual financial responsibility for every taxpayer in India. As we navigate the assessment cycle for AY 2026-27 (which covers the income earned during the Financial Year FY 2025-26), staying updated on tax timelines is the only foolproof way to safeguard your hard earned money from avoidable penalties and complex legal bottlenecks.

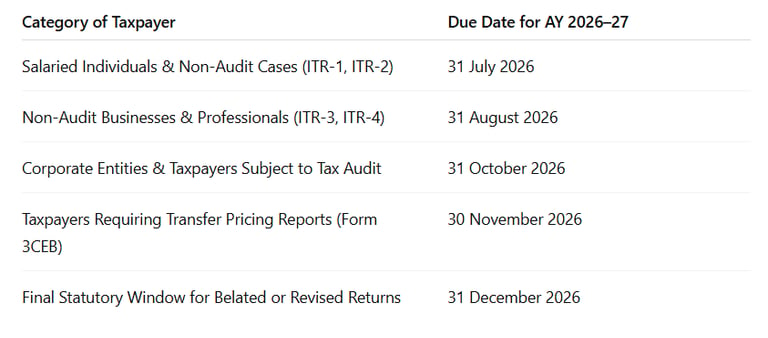

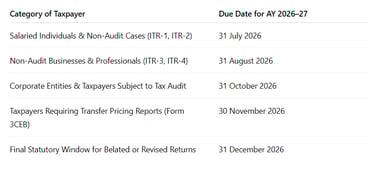

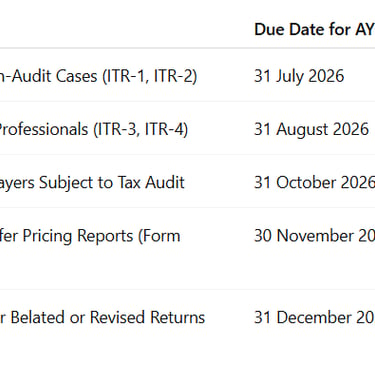

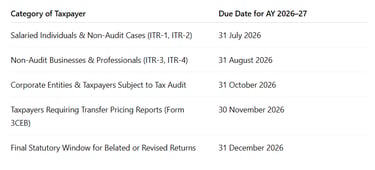

Important ITR Filing Deadlines for AY 2026-27

To prevent structural penalties, you must submit your tax returns on or before specific dates determined by your source of income and corporate categorization.

Following recent updates aimed at easing compliance pressures, the statutory timelines for this assessment year are structured as follows:

Understanding Late Fees Under Section 234F

If you miss your initial respective tax category deadline, the Income Tax Department allows you to file what is known as a belated return under Section 139(4). While this keeps you within the formal digital network, it automatically activates a mandatory late fee structure regulated by Section 234F.

The fine limits are systematically tiered based on your final net taxable income:

Total Taxable Income Above Rs. 5 Lakh: If your total net income (after applicable deductions) exceeds Rs. 5,00,000, a flat late filing penalty of Rs. 5,000 is levied.

Total Taxable Income Up to Rs. 5 Lakh: For taxpayers whose total taxable income stays at or below Rs. 5,00,000, the late fee is legally capped at a maximum of Rs. 1,000.

Gross Total Income Below Basic Exemption Limit: If your gross total income is below the fundamental exemption threshold (e.g., Rs. 3,00,000 under the default New Tax Regime), you are generally exempted from paying a late fee under Section 234F, provided you do not trigger special criteria like high-value electricity consumption or foreign asset ownership.

Fact Check Note: While outdated financial articles might still mention late fees scaling up to Rs. 10,000 for filings done closer to March, structural tax amendments have capped the absolute maximum Section 234F penalty at Rs. 5,000 since the financial year 2021.

Additional Financial Consequences of Late Filing

Missing the deadline brings consequences that stretch far beyond a one-time flat penalty. Delayed submissions directly impact your broad portfolio:

1. Interest Liabilities Under Section 234A

If you have outstanding tax liabilities that were not settled via Advance Tax or Self-Assessment Tax before your original deadline, Section 234A imposes a mandatory interest charge of 1% per month (or any part of a month). This interest accumulates cumulatively until the exact day you file the ITR and clear your outstanding balance.

2. Elimination of Right to Carry Forward Losses

One of the most damaging setbacks for active investors and business owners who delay their filings is losing the ability to carry forward certain losses. If your return is filed late, you forfeit the right to pass on business losses or capital losses (short-term or long-term) to subsequent fiscal years to offset future gains.

3. Delayed Tax Refunds and Loss of Interest

If your TDS deductions exceed your actual tax liability, filing your return late naturally stalls your processing cycle. Consequently, your tax refund is pushed back significantly, and you risk losing out on a portion of the interest otherwise payable by the department on delayed refunds.

4. Restrictions on Choosing the Old Tax Regime

Under current tax rules, if you do not file your income tax return within the original statutory deadline, you lose the option to select the Old Tax Regime. The system restricts late filers to the default New Tax Regime, which could result in a higher tax payout if you rely heavily on traditional exemptions like HRA or Section 80C.

Compliance Requirements for Companies and Firms

Corporate entities, LLPs, and partnership firms face rigid regulatory oversight, where filing deviations carry steep commercial consequences:

Partnership Firms & Tax Audits: Missing the structural tax audit deadlines or failing to furnish required accounting reports can yield distinct penalties under Section 271B, calculated at 0.5% of total turnover or Rs. 1,50,000, whichever is lower.

Private Limited Companies: Corporate delays generate intense scrutiny. Inaccurate reporting or systemic failures to submit returns on time can trigger penalties ranging from 30% to 60% of the underlying tax sought to be evaded, alongside severe corporate governance implications.

Charitable Trusts (ITR-7): Delayed filings put the vital tax-exempt status of religious, charitable, or educational institutions at risk under systemic trust verification rules.

What Happens if You Miss the December 31st Deadline?

Once the calendar hits December 31, 2026, the window to file a regular belated return for AY 2026-27 closes entirely. Beyond this date, you have only two narrow operational pathways left to regularize your taxes:

Updated Return (Section 139(8A)): You can choose to file an "Updated Return" (Form ITR-U). This pathway is open for up to 24 months from the end of the relevant assessment year. However, it comes with a condition: you must pay an additional compliance premium consisting of 25% to 50% extra tax and interest on top of your existing dues, and it cannot be used to claim a refund or report a loss.

Condonation of Delay: For extreme, highly documented scenarios (such as critical medical emergencies, severe accidents, or systemic natural disasters), you can file a formal application under Section 119(2)(b) to seek special permission from the income tax authorities to submit a late return.

Conclusion

Filing your tax return on time is about more than just avoiding a Rs. 5,000 penalty. A clean track record of timely ITR submissions is highly valued by banking institutions and global embassies, making it an absolute necessity when applying for home loans, business lines of credit, or international visas.

By prioritizing your respective July or August deadline, you maximize your legal tax benefits, retain the right to carry forward losses, and secure long-term financial peace of mind.

Frequently Asked Questions (FAQs)

Q1: What is the maximum late filing penalty for AY 2026-27?

The maximum fine under Section 234F is Rs. 5,000 if your total taxable income exceeds Rs. 5 lakh. For individuals whose taxable income is Rs. 5 lakh or less, the penalty is strictly capped at Rs. 1,000.

Q2: Am I liable for a penalty if my income is entirely below the basic taxable limit?

No. If your gross total income is below the basic exemption threshold, the Section 234F late fee does not apply. However, you must still file on time if you meet specific criteria, such as depositing over Rs. 1 crore in current accounts or spending over Rs. 2 lakh on international travel.

Q3: Can I correct an error in my tax return if I already filed it?

Yes, you can file a Revised Return under Section 139(5) to correct mistakes made in your original filing. For AY 2026-27, the deadline to submit a revised return is December 31, 2026.

Q4: Can I carry forward stock market capital losses if I file a belated return?

No. To carry forward capital losses or business losses to future assessment years, the law mandates that your original ITR must be submitted before the initial due date. Belated returns do not allow the carry forward of these losses.

Get Professional Help with Your Taxes

Do not let complicated compliance structures and approaching deadlines cause you stress. Let the certified tax experts at Filing4U handle your complete end-to-end tax filing while you focus on scaling your career and business operations.

Call us +91 7980984206

Filing your Income Tax Return (ITR) is a critical annual financial responsibility for every taxpayer in India. As we navigate the assessment cycle for AY 2026-27 (which covers the income earned during the Financial Year FY 2025-26), staying updated on tax timelines is the only foolproof way to safeguard your hard earned money from avoidable penalties and complex legal bottlenecks.

Important ITR Filing Deadlines for AY 2026-27

To prevent structural penalties, you must submit your tax returns on or before specific dates determined by your source of income and corporate categorization.

Following recent updates aimed at easing compliance pressures, the statutory timelines for this assessment year are structured as follows:

Understanding Late Fees Under Section 234F

If you miss your initial respective tax category deadline, the Income Tax Department allows you to file what is known as a belated return under Section 139(4). While this keeps you within the formal digital network, it automatically activates a mandatory late fee structure regulated by Section 234F.

The fine limits are systematically tiered based on your final net taxable income:

Total Taxable Income Above Rs. 5 Lakh: If your total net income (after applicable deductions) exceeds Rs. 5,00,000, a flat late filing penalty of Rs. 5,000 is levied.

Total Taxable Income Up to Rs. 5 Lakh: For taxpayers whose total taxable income stays at or below Rs. 5,00,000, the late fee is legally capped at a maximum of Rs. 1,000.

Gross Total Income Below Basic Exemption Limit: If your gross total income is below the fundamental exemption threshold (e.g., Rs. 3,00,000 under the default New Tax Regime), you are generally exempted from paying a late fee under Section 234F, provided you do not trigger special criteria like high-value electricity consumption or foreign asset ownership.

Fact Check Note: While outdated financial articles might still mention late fees scaling up to Rs. 10,000 for filings done closer to March, structural tax amendments have capped the absolute maximum Section 234F penalty at Rs. 5,000 since the financial year 2021.

Additional Financial Consequences of Late Filing

Missing the deadline brings consequences that stretch far beyond a one-time flat penalty. Delayed submissions directly impact your broad portfolio:

1. Interest Liabilities Under Section 234A

If you have outstanding tax liabilities that were not settled via Advance Tax or Self-Assessment Tax before your original deadline, Section 234A imposes a mandatory interest charge of 1% per month (or any part of a month). This interest accumulates cumulatively until the exact day you file the ITR and clear your outstanding balance.

2. Elimination of Right to Carry Forward Losses

One of the most damaging setbacks for active investors and business owners who delay their filings is losing the ability to carry forward certain losses. If your return is filed late, you forfeit the right to pass on business losses or capital losses (short-term or long-term) to subsequent fiscal years to offset future gains.

3. Delayed Tax Refunds and Loss of Interest

If your TDS deductions exceed your actual tax liability, filing your return late naturally stalls your processing cycle. Consequently, your tax refund is pushed back significantly, and you risk losing out on a portion of the interest otherwise payable by the department on delayed refunds.

4. Restrictions on Choosing the Old Tax Regime

Under current tax rules, if you do not file your income tax return within the original statutory deadline, you lose the option to select the Old Tax Regime. The system restricts late filers to the default New Tax Regime, which could result in a higher tax payout if you rely heavily on traditional exemptions like HRA or Section 80C.

Compliance Requirements for Companies and Firms

Corporate entities, LLPs, and partnership firms face rigid regulatory oversight, where filing deviations carry steep commercial consequences:

Partnership Firms & Tax Audits: Missing the structural tax audit deadlines or failing to furnish required accounting reports can yield distinct penalties under Section 271B, calculated at 0.5% of total turnover or Rs. 1,50,000, whichever is lower.

Private Limited Companies: Corporate delays generate intense scrutiny. Inaccurate reporting or systemic failures to submit returns on time can trigger penalties ranging from 30% to 60% of the underlying tax sought to be evaded, alongside severe corporate governance implications.

Charitable Trusts (ITR-7): Delayed filings put the vital tax-exempt status of religious, charitable, or educational institutions at risk under systemic trust verification rules.

What Happens if You Miss the December 31st Deadline?

Once the calendar hits December 31, 2026, the window to file a regular belated return for AY 2026-27 closes entirely. Beyond this date, you have only two narrow operational pathways left to regularize your taxes:

Updated Return (Section 139(8A)): You can choose to file an "Updated Return" (Form ITR-U). This pathway is open for up to 24 months from the end of the relevant assessment year. However, it comes with a condition: you must pay an additional compliance premium consisting of 25% to 50% extra tax and interest on top of your existing dues, and it cannot be used to claim a refund or report a loss.

Condonation of Delay: For extreme, highly documented scenarios (such as critical medical emergencies, severe accidents, or systemic natural disasters), you can file a formal application under Section 119(2)(b) to seek special permission from the income tax authorities to submit a late return.

Conclusion

Filing your tax return on time is about more than just avoiding a Rs. 5,000 penalty. A clean track record of timely ITR submissions is highly valued by banking institutions and global embassies, making it an absolute necessity when applying for home loans, business lines of credit, or international visas.

By prioritizing your respective July or August deadline, you maximize your legal tax benefits, retain the right to carry forward losses, and secure long-term financial peace of mind.

Frequently Asked Questions (FAQs)

Q1: What is the maximum late filing penalty for AY 2026-27?

The maximum fine under Section 234F is Rs. 5,000 if your total taxable income exceeds Rs. 5 lakh. For individuals whose taxable income is Rs. 5 lakh or less, the penalty is strictly capped at Rs. 1,000.

Q2: Am I liable for a penalty if my income is entirely below the basic taxable limit?

No. If your gross total income is below the basic exemption threshold, the Section 234F late fee does not apply. However, you must still file on time if you meet specific criteria, such as depositing over Rs. 1 crore in current accounts or spending over Rs. 2 lakh on international travel.

Q3: Can I correct an error in my tax return if I already filed it?

Yes, you can file a Revised Return under Section 139(5) to correct mistakes made in your original filing. For AY 2026-27, the deadline to submit a revised return is December 31, 2026.

Q4: Can I carry forward stock market capital losses if I file a belated return?

No. To carry forward capital losses or business losses to future assessment years, the law mandates that your original ITR must be submitted before the initial due date. Belated returns do not allow the carry forward of these losses.

Get Professional Help with Your Taxes

Do not let complicated compliance structures and approaching deadlines cause you stress. Let the certified tax experts at Filing4U handle your complete end-to-end tax filing while you focus on scaling your career and business operations.

Call us +91 7980984206

Copyright 2026 Filing4u. All Rights Reserved. Powered by Digital Nari

Get In Touch

Tel : +91 79809 84206

Email : info@filing4u.com

Locations : Kolkata | Bangalore | Mumbai

H.O: Industry House, 10, Camac St, Elgin, Kolkata, West Bengal 700017