ITR-3 Filing is Now Live for AY 2026–27: Everything Traders & Business Owners Must Know

ITR-3 filing for Assessment Year (AY) 2026–27 is officially open on the Income Tax portal. If you have income from F&O trading, intraday transactions, or a business/profession, ITR-3 is your mandatory form. Filing it correctly protects you from tax notices, optimizes your deductions and prevents costly errors. This guide covers exactly what you need to know.

Sneha Das

7/9/202612 min read

The Income Tax Department has enabled ITR-3 filing for AY 2026–27, following the earlier rollout of ITR-1, ITR-2, and ITR-4. For traders, freelancers, and small business owners, the filing window is officially open and every day you wait brings you closer to the peak tax season rush.

Filing ITR-3 requires a high level of precision compared to simpler forms like ITR-1. It demands accurate classification of income heads, proper loss set-off sequencing, tax regime selection backed by real numbers, and audit-readiness if you breach turnover thresholds. Mistakes here frequently result in a "defective return" notice or an inflated tax bill.

Who Should File ITR-3?

ITR-3 applies to individuals and Hindu Undivided Families (HUFs) who have:

Income from a proprietary business or profession

F&O (Futures & Options) trading income or losses

Intraday equity trading income (legally treated as speculative business income)

A combination of salary, capital gains, and business income

Rental income alongside active business income

Crucial Warning for Traders:

If you traded in derivatives even once during FY 2025–26 and incurred a loss, you must file ITR-3, not ITR-2. Many retail traders make the mistake of using simpler forms, which instantly disqualifies them from carrying forward their losses to offset future trading profits.

Key Changes & Updates for AY 2026–27

Before preparing your sheets, ensure your data accounts for the following updates this assessment year:

Revised New Tax Regime Slabs: The restructured slabs apply as the default choice. Ensure your calculations are based on the updated structural limits.

Revised STT Rates: Securities Transaction Tax (STT) rates on F&O trades have shifted. Verify that your Profit & Loss (P&L) statements accurately reflect these changes before filing.

Turnover Calculation Framework: F&O turnover computation must follow ICAI guidelines: the absolute value of profits + losses, rather than net settlement amounts.

Audit Thresholds: The tax audit threshold for business income without presumptive taxation remains at ₹1 crore, subject to meeting digital transaction minimums.

Regime Optimization: A meticulous comparison between the Old and New Tax Regimes is highly critical for traders carrying business deductions or variable income.

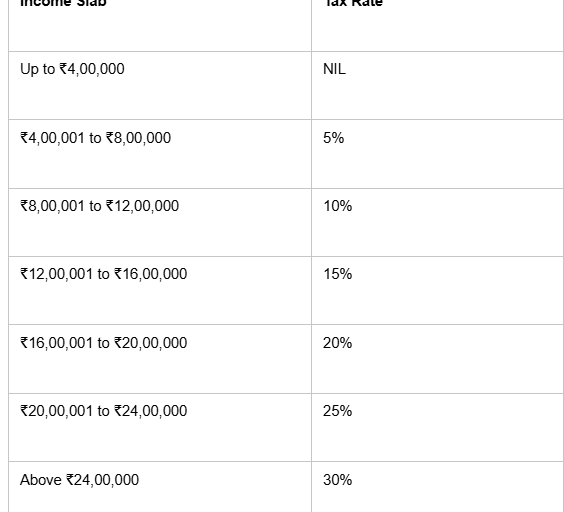

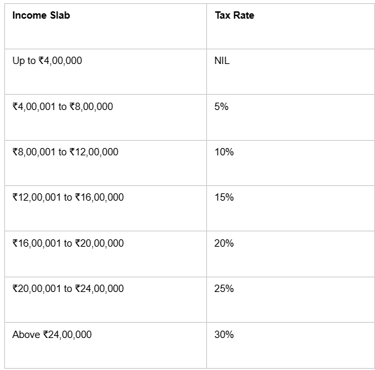

Official Income Tax Slabs for FY 2025–26 (AY 2026–27)

If your income surpasses the zero-tax rebate thresholds, your progressive tax liability is computed using the following slab rates:

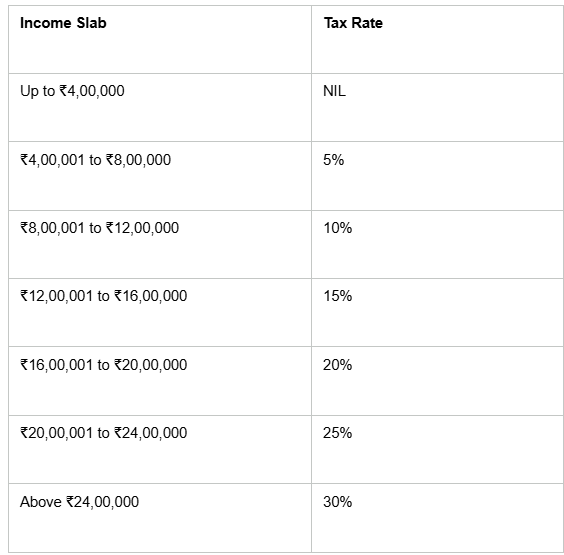

New Tax Regime Slabs (Default)

The 5 Biggest Mistakes Traders Make While Filing ITR-3

1. Filing the Wrong ITR Form

Intraday and F&O income is classified as business income. Attempting to report F&O losses under ITR-2 results in a defective return notice and the rejection of your carry-forward claims.

2. Blindly Selecting a Tax Regime

Your final liability can shift significantly based on your regime selection. The right choice relies directly on your specific deductions, HRA allocations, Section 80C investments, and eligible business expenses.

3. Mismanaging Loss Set-Off Sequences

Business losses, speculative losses, and capital losses each follow distinct set-off and carry forward timelines. Processing them without proper sequencing can lead to paying more tax than legally required.

4. Incorrect Turnover Computation

For F&O trading, turnover is not your net profit or loss. It is the cumulative sum of the absolute values of all trade profits and losses combined. Understating this volume can flag your profile for scrutiny.

5. Ignoring Historic Income Tax Notices

If you received an outstanding tax notice for AY 2024–25 or earlier, it should be addressed before submitting your current filing. Unresolved compliance flags tend to compound over time.

Essential Deductions to Lower Your Tax (Old Regime)

If your income structure makes the Old Regime more profitable, these are your primary financial tools for reducing your taxable income:

Section 80C (The Foundation): Allows a total deduction of up to ₹1.5 Lakh. This includes your Employee Provident Fund (EPF), Public Provident Fund (PPF), life insurance premiums, and Equity-Linked Savings Schemes (ELSS).

Section 80D (Health Insurance): Claim up to ₹25,000 for a premium paid for yourself, spouse, and children, and an additional ₹50,000 if you pay for your senior citizen parents.

Section 80E (Education Loans): As a young professional, you can deduct the entire interest amount paid on loans taken for higher education for up to 8 consecutive years.

House Rent Allowance (HRA): If you live in a rented home, you can claim tax exemptions based on your actual rent paid, metro vs. non-metro location, and basic salary structure.

What Filing4u Does Differently

Most platforms provide tax software; we provide hands-on expertise. When you file your ITR-3 with Filing4u Consultancy, your file is handled via direct human evaluation:

Dedicated Tax Experts: You are paired with a dedicated tax professional—not a chatbot or automated script.

Accurate Trade Categorization: Precise management of F&O income, intraday trades, and speculative vs. non-speculative classification.

Side-by-side Regime Comparison: Custom calculations based on your real trading numbers, not broad industry averages.

Optimized Loss Adjustments: Correct execution of loss set-offs and carry-forward tracking across all applicable heads.

Full Audit Support: Comprehensive documentation and assistance if your operational turnover triggers a statutory tax audit.

Notice Management: Expert response assistance for any prior or incoming clarifications issued by the Income Tax Department.

How to Get Started with Your Filing

Getting your ITR-3 prepared and filed with Filing4u is straightforward:

1.Connect & Share: Step 1.

Visit our portal or call our support line to share your trading statements, Form 26AS, AIS, and basic income documents.

2.Expert Review: Step 2.

Our assigned tax expert reviews your data, calculates your correct turnover, and prepares your return with accuracy checks.

3.Approval:Step 3.

You review the completed computations, select the optimal tax regime, and provide your formal sign-off.

4.Filing & Verification: Step 4.

We submit your ITR-3 directly to the official portal and deliver your formal filing acknowledgment copy.

Frequently Asked Question (FAQ’s)

Q1: Is income up to ₹12 lakh completely tax-free under the New Tax Regime?

Answer: Yes. Under the updated rules for FY 2025–26, resident individuals with a net taxable income up to ₹12,00,000 pay zero income tax. Even though the slabs levy a 5% and 10% tax on components above ₹4 Lakhs, the enhanced Section 87A rebate of up to ₹60,000 wipes out your total tax liability entirely.

Q2: What is the maximum income limit for zero tax for salaried employees?

Answer: For salaried individuals and pensioners, the effective zero-tax threshold is ₹12,75,000. This is achieved by combining the ₹75,000 Standard Deduction (automatically deducted from your gross salary) and the ₹60,000 Section 87A tax rebate available on net taxable income up to ₹12 Lakhs.

Q3: How is Marginal Relief calculated if my income slightly exceeds ₹12 Lakhs?

Answer: If your net taxable income is marginally over ₹12 Lakhs (say, ₹12,10,000), you no longer lose the entire Section 87A rebate. Instead, Marginal Relief steps in to ensure that the extra tax you pay cannot exceed the extra income you earned over the ₹12 Lakh threshold.

For instance, on an income of ₹12.10 Lakhs, the raw tax calculated via slabs is ₹61,500. Since the excess income over ₹12 Lakhs is only ₹10,000, your final tax liability is restricted to just ₹10,000, plus a 4% health & education cess.

Q4: Which deductions are allowed under the New Tax Regime for FY 2025–26?

Answer: The New Tax Regime disallows popular deductions like Section 80C (PPF, ELSS, LIC), Section 80D (Health Insurance), and HRA (House Rent Allowance). However, you can still claim the following:

Standard Deduction of ₹75,000 (for salaried individuals).

Deduction on employer's contribution to NPS under Section 80CCD(2).

Additional tax deductions through child-focused investment plans like NPS Vatsalya.

Q5: Can I switch back to the Old Tax Regime when filing my ITR?

Answer: Yes, the Old Tax Regime remains optional. Salaried individuals without business income have the flexibility to switch between the Old and New tax regimes every financial year at the time of filing their Income Tax Return (ITR). However, if you have business or professional income (like F&O trading), you get only a one-time option to opt out of the default New Tax Regime.

File Now. File Right.

The July 31 deadline arrives quickly, especially when actively managing open market positions. Avoid relying on generic automated software that struggles to process complex derivative trading books. ITR-3 is your mandatory form—file it with professionals who understand the numbers.

Conclusion

Smart tax planning is far more than an annual compliance task; it is a strategic exercise in wealth creation. For young professionals, freelancers, and active traders alike, the choice between the Old and New Tax Regimes can significantly impact your financial growth. By starting your tax planning early in the financial year, tracking your investment options carefully, and precisely categorizing every income head especially complex ones like F&O and intraday trading you can legally minimize your liability and build a stronger, more secure financial foundation for the future.

Need Expert Help?

At Filing4U, we take the complexity out of tax planning, investment structuring, and ITR filing so you can stay completely focused on scaling your career or growing your portfolio.

Get in touch with our certified tax professionals today for seamless, accurate and completely stress free tax solutions:

Call us +91 7980984206

Need expert help? Connect with Filing4U for Expert Legal & Tax Support

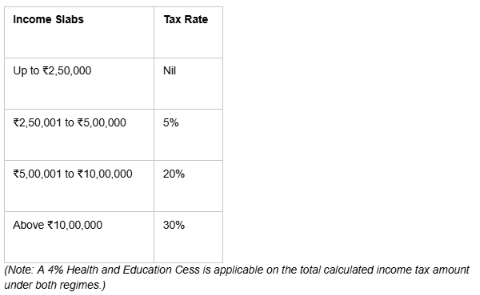

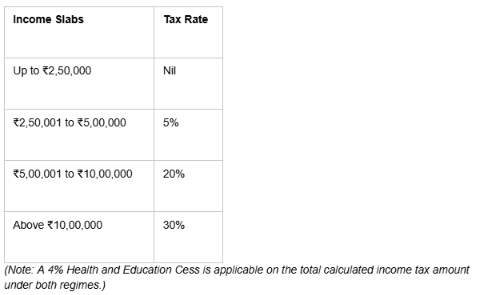

Old Tax Regime Slabs (Optional)

The Income Tax Department has enabled ITR-3 filing for AY 2026–27, following the earlier rollout of ITR-1, ITR-2, and ITR-4. For traders, freelancers, and small business owners, the filing window is officially open and every day you wait brings you closer to the peak tax season rush.

Filing ITR-3 requires a high level of precision compared to simpler forms like ITR-1. It demands accurate classification of income heads, proper loss set-off sequencing, tax regime selection backed by real numbers, and audit-readiness if you breach turnover thresholds. Mistakes here frequently result in a "defective return" notice or an inflated tax bill.

Who Should File ITR-3?

ITR-3 applies to individuals and Hindu Undivided Families (HUFs) who have:

Income from a proprietary business or profession

F&O (Futures & Options) trading income or losses

Intraday equity trading income (legally treated as speculative business income)

A combination of salary, capital gains, and business income

Rental income alongside active business income

Crucial Warning for Traders:

If you traded in derivatives even once during FY 2025–26 and incurred a loss, you must file ITR-3, not ITR-2. Many retail traders make the mistake of using simpler forms, which instantly disqualifies them from carrying forward their losses to offset future trading profits.

Key Changes & Updates for AY 2026–27

Before preparing your sheets, ensure your data accounts for the following updates this assessment year:

Revised New Tax Regime Slabs: The restructured slabs apply as the default choice. Ensure your calculations are based on the updated structural limits.

Revised STT Rates: Securities Transaction Tax (STT) rates on F&O trades have shifted. Verify that your Profit & Loss (P&L) statements accurately reflect these changes before filing.

Turnover Calculation Framework: F&O turnover computation must follow ICAI guidelines: the absolute value of profits + losses, rather than net settlement amounts.

Audit Thresholds: The tax audit threshold for business income without presumptive taxation remains at ₹1 crore, subject to meeting digital transaction minimums.

Regime Optimization: A meticulous comparison between the Old and New Tax Regimes is highly critical for traders carrying business deductions or variable income.

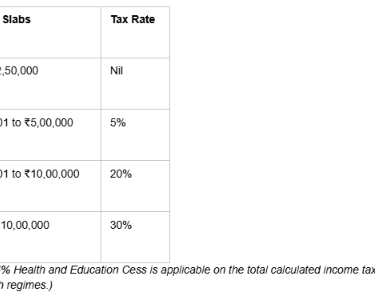

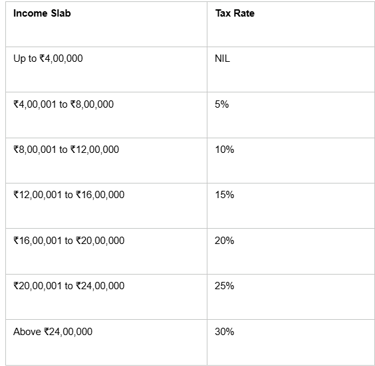

Official Income Tax Slabs for FY 2025–26 (AY 2026–27)

If your income surpasses the zero-tax rebate thresholds, your progressive tax liability is computed using the following slab rates:

New Tax Regime Slabs (Default)

The 5 Biggest Mistakes Traders Make While Filing ITR-3

1. Filing the Wrong ITR Form

Intraday and F&O income is classified as business income. Attempting to report F&O losses under ITR-2 results in a defective return notice and the rejection of your carry-forward claims.

2. Blindly Selecting a Tax Regime

Your final liability can shift significantly based on your regime selection. The right choice relies directly on your specific deductions, HRA allocations, Section 80C investments, and eligible business expenses.

3. Mismanaging Loss Set-Off Sequences

Business losses, speculative losses, and capital losses each follow distinct set-off and carry forward timelines. Processing them without proper sequencing can lead to paying more tax than legally required.

4. Incorrect Turnover Computation

For F&O trading, turnover is not your net profit or loss. It is the cumulative sum of the absolute values of all trade profits and losses combined. Understating this volume can flag your profile for scrutiny.

5. Ignoring Historic Income Tax Notices

If you received an outstanding tax notice for AY 2024–25 or earlier, it should be addressed before submitting your current filing. Unresolved compliance flags tend to compound over time.

Essential Deductions to Lower Your Tax (Old Regime)

If your income structure makes the Old Regime more profitable, these are your primary financial tools for reducing your taxable income:

Section 80C (The Foundation): Allows a total deduction of up to ₹1.5 Lakh. This includes your Employee Provident Fund (EPF), Public Provident Fund (PPF), life insurance premiums, and Equity-Linked Savings Schemes (ELSS).

Section 80D (Health Insurance): Claim up to ₹25,000 for a premium paid for yourself, spouse, and children, and an additional ₹50,000 if you pay for your senior citizen parents.

Section 80E (Education Loans): As a young professional, you can deduct the entire interest amount paid on loans taken for higher education for up to 8 consecutive years.

House Rent Allowance (HRA): If you live in a rented home, you can claim tax exemptions based on your actual rent paid, metro vs. non-metro location, and basic salary structure.

What Filing4u Does Differently

Most platforms provide tax software; we provide hands-on expertise. When you file your ITR-3 with Filing4u Consultancy, your file is handled via direct human evaluation:

Dedicated Tax Experts: You are paired with a dedicated tax professional—not a chatbot or automated script.

Accurate Trade Categorization: Precise management of F&O income, intraday trades, and speculative vs. non-speculative classification.

Side-by-side Regime Comparison: Custom calculations based on your real trading numbers, not broad industry averages.

Optimized Loss Adjustments: Correct execution of loss set-offs and carry-forward tracking across all applicable heads.

Full Audit Support: Comprehensive documentation and assistance if your operational turnover triggers a statutory tax audit.

Notice Management: Expert response assistance for any prior or incoming clarifications issued by the Income Tax Department.

How to Get Started with Your Filing

Getting your ITR-3 prepared and filed with Filing4u is straightforward:

1.Connect & Share: Step 1.

Visit our portal or call our support line to share your trading statements, Form 26AS, AIS, and basic income documents.

2.Expert Review: Step 2.

Our assigned tax expert reviews your data, calculates your correct turnover, and prepares your return with accuracy checks.

3.Approval:Step 3.

You review the completed computations, select the optimal tax regime, and provide your formal sign-off.

4.Filing & Verification: Step 4.

We submit your ITR-3 directly to the official portal and deliver your formal filing acknowledgment copy.

Frequently Asked Question (FAQ’s)

Q1: Is income up to ₹12 lakh completely tax-free under the New Tax Regime?

Answer: Yes. Under the updated rules for FY 2025–26, resident individuals with a net taxable income up to ₹12,00,000 pay zero income tax. Even though the slabs levy a 5% and 10% tax on components above ₹4 Lakhs, the enhanced Section 87A rebate of up to ₹60,000 wipes out your total tax liability entirely.

Q2: What is the maximum income limit for zero tax for salaried employees?

Answer: For salaried individuals and pensioners, the effective zero-tax threshold is ₹12,75,000. This is achieved by combining the ₹75,000 Standard Deduction (automatically deducted from your gross salary) and the ₹60,000 Section 87A tax rebate available on net taxable income up to ₹12 Lakhs.

Q3: How is Marginal Relief calculated if my income slightly exceeds ₹12 Lakhs?

Answer: If your net taxable income is marginally over ₹12 Lakhs (say, ₹12,10,000), you no longer lose the entire Section 87A rebate. Instead, Marginal Relief steps in to ensure that the extra tax you pay cannot exceed the extra income you earned over the ₹12 Lakh threshold.

For instance, on an income of ₹12.10 Lakhs, the raw tax calculated via slabs is ₹61,500. Since the excess income over ₹12 Lakhs is only ₹10,000, your final tax liability is restricted to just ₹10,000, plus a 4% health & education cess.

Q4: Which deductions are allowed under the New Tax Regime for FY 2025–26?

Answer: The New Tax Regime disallows popular deductions like Section 80C (PPF, ELSS, LIC), Section 80D (Health Insurance), and HRA (House Rent Allowance). However, you can still claim the following:

Standard Deduction of ₹75,000 (for salaried individuals).

Deduction on employer's contribution to NPS under Section 80CCD(2).

Additional tax deductions through child-focused investment plans like NPS Vatsalya.

Q5: Can I switch back to the Old Tax Regime when filing my ITR?

Answer: Yes, the Old Tax Regime remains optional. Salaried individuals without business income have the flexibility to switch between the Old and New tax regimes every financial year at the time of filing their Income Tax Return (ITR). However, if you have business or professional income (like F&O trading), you get only a one-time option to opt out of the default New Tax Regime.

File Now. File Right.

The July 31 deadline arrives quickly, especially when actively managing open market positions. Avoid relying on generic automated software that struggles to process complex derivative trading books. ITR-3 is your mandatory form—file it with professionals who understand the numbers.

Conclusion

Smart tax planning is far more than an annual compliance task; it is a strategic exercise in wealth creation. For young professionals, freelancers, and active traders alike, the choice between the Old and New Tax Regimes can significantly impact your financial growth. By starting your tax planning early in the financial year, tracking your investment options carefully, and precisely categorizing every income head especially complex ones like F&O and intraday trading you can legally minimize your liability and build a stronger, more secure financial foundation for the future.

Need Expert Help?

At Filing4U, we take the complexity out of tax planning, investment structuring, and ITR filing so you can stay completely focused on scaling your career or growing your portfolio.

Get in touch with our certified tax professionals today for seamless, accurate and completely stress free tax solutions:

Call us +91 7980984206

Need expert help? Connect with Filing4U for Expert Legal & Tax Support

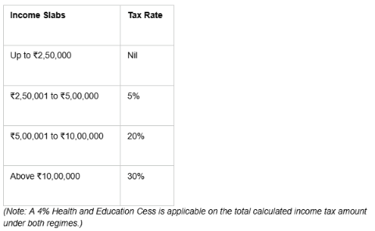

Old Tax Regime Slabs (Optional)

Copyright 2026 Filing4u. All Rights Reserved. Powered by Digital Nari

Get In Touch

Tel : +91 79809 84206

Email : info@filing4u.com

Locations : Kolkata | Bangalore | Mumbai

H.O: Industry House, 10, Camac St, Elgin, Kolkata, West Bengal 700017