15 Common Mistakes to Avoid While Filing ITR for FY 2025-26 (AY 2026-27)

The most critical mistakes to avoid while filing your ITR for AY 2026-27 are failing to cross verify data with your AIS and Form 26AS, filing before June 15 (before your Form 16 fully updates on the portal), selecting the wrong ITR form for your income sources (like using ITR-1 instead of ITR-3 for crypto or F&O trading), omitting exempt incomes like PPF or dividend earnings, and forgetting to pre validate your bank account, all of which guarantee automatic tax notices or delayed refunds.

Sneha Das

5/26/202610 min read

Filing your Income Tax Return (ITR) can feel like a daunting task, but it is a critical part of your financial responsibility. For Financial Year (FY) 2025-26 (Assessment Year (AY) 2026-27), the filing season comes with specific compliance updates, strict deadlines, and new tax structures that taxpayers must navigate carefully.

1. Choosing the Wrong ITR Form

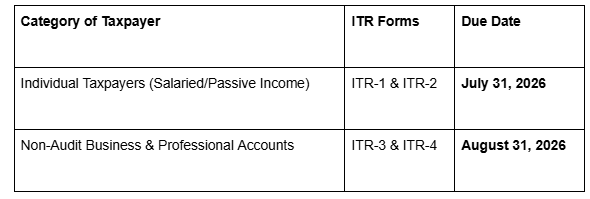

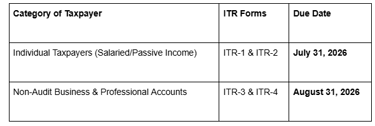

Selecting the incorrect ITR form is one of the most frequent errors. For instance, ITR-1 (Sahaj) is meant strictly for resident salaried individuals with a total income below ₹50 lakh and no capital gains, while ITR-3 or ITR-4 (Sugam) is mandatory for individuals with income from a business or profession. Filing the wrong form can result in your return being flagged as defective under Section 139(9).

2. Quoting the Incorrect Assessment Year (AY)

For the financial year starting April 1, 2025, and ending March 31, 2026 (FY 2025-26), the correct corresponding Assessment Year is AY 2026-27. Confusing these two years is a basic error that can lead to erroneous double taxation data, delayed processing, or unnecessary penalties.

3. Errors in Personal, PAN, and Bank Information

Ensure your name, Permanent Account Number (PAN), Aadhaar number, mobile number, and email address match your official government records exactly. Additionally, if you are expecting a tax refund, double check your bank account number and IFSC code. Incorrect or unvalidated bank details are the primary reason for delayed or failed tax refunds.

4. Failing to Disclose All Income Sources

Taxpayers frequently forget to report "secondary" or passive income. You must legally disclose interest earned from savings accounts, fixed deposits (FDs), recurring deposits, rental income, and even tax-exempt income (like agricultural income or PPF interest).

Important Note: Even if a specific income source is completely exempt from tax, it must still be declared under the appropriate exempt income schedules in your return.

5. Overlooking Capital Gains Disclosure

While long-term capital gains (LTCG) on equity shares or equity-oriented mutual funds are exempt up to a specific statutory threshold (e.g., ₹1.25 lakh under updated slabs), you are still legally required to disclose these transactions. Failing to report capital gains, whether short-term or long-term will trigger an automated data mismatch notice.

6. Ignoring Form 26AS Reconciliation

Before submitting your return, you must reconcile your income and Tax Deducted at Source (TDS) with your Form 26AS. If your employer, bank, or a client has deducted tax but it does not reflect in your Form 26AS ledger, you will not receive the tax credit. This discrepancy routinely leads to a higher tax demand or a severely reduced refund.

7. Not Checking AIS and TIS

The Income Tax Department relies heavily on the Annual Information Statement (AIS) and Taxpayer Information Summary (TIS). These documents provide a comprehensive view of your high-value financial transactions, including stock market trades, mutual fund dividend distributions, and foreign remittances. Ensure the pre-filled values in your ITR match your actual bank statements and brokerage summaries.

8. Mismanaging Multiple Form 16s

If you changed jobs during the financial year, you will receive a Form 16 from both your previous and current employers. When filing, you must aggregate the salary income, allowances, and perquisites from both employers. Failing to combine this data often results in an underpayment of tax, as both employers may have independently applied basic tax exemptions.

9. Forgetting to Claim HRA Separately

If you forgot to submit your rent receipts or rent agreement to your corporate HR department before the year end payroll window closed, you can still claim the House Rent Allowance (HRA) exemption directly while filing your ITR, provided you have your landlord's PAN.

10. Missing Out on Eligible Deductions

Taxpayers frequently overlook valid deductions that can significantly lower their net taxable income. Ensure you have calculated all eligible expenditures, medical insurance premiums, educational loan interest and registered charitable donations before finalizing your submission.

11. Neglecting Advance Tax Payments

To avoid interest liabilities under Sections 234B and 234C, your estimated tax liability exceeding ₹10,000 must be paid in four installments throughout the fiscal year (June 15, September 15, December 15, and March 15). Shortfalls or delays in Advance Tax attract a 1% monthly interest penalty.

12. Misunderstanding NSC Interest Taxation

Interest earned on National Savings Certificates (NSC) is not completely tax-free. While the interest accrued can generally be reinvested and claimed as a deduction under Section 80C for the initial years, it must still be systematically reported each year under "Income from Other Sources."

13. Missing the 30-Day E-Verification Window

Filing your return online is only half the job. You must successfully e-verify your ITR within 30 days of submission via Aadhaar OTP, Net Banking, or an Electronic Verification Code (EVC). If you cannot e-verify digitally, a signed physical copy of your ITR-V must reach the Centralized Processing Cell (CPC) in Bengaluru within that strict 30-day window, or your return will be treated as invalid.

14. Failing to File Schedule AL (Assets and Liabilities)

If your total taxable income exceeds ₹50 lakh, you are mandatorily required to fill out Schedule AL. This requires a comprehensive disclosure of your physical assets (immovable properties, vehicles, bullion, etc.) along with any corresponding financial liabilities or loans.

15. Not Disclosing Foreign Assets and Income

Resident Indians must report all foreign income, foreign bank accounts and offshore assets, including global stocks, foreign mutual funds, or foreign corporate ESOPs—in Schedule FA. This is a mandatory disclosure requirement even if the income generated from these assets is not taxable within India. Non-disclosure carries severe penalties under the Black Money Act.

Important Deadlines for FY 2025-26 (AY 2026-27)

Conclusion

Avoiding these common tax filing mistakes saves you time, prevents unexpected tax demands, and keeps your financial record clean. A little preparation goes a long way toward ensuring an effortless filing season. For a completely stress-free experience, it is always recommended to compile your documents and start your filing process early to beat the last minute rush.

Frequently Asked Questions (FAQs)

Q1. What happens if I file the wrong ITR form?

If you select an incorrect form, the Income Tax Department will issue a notice under Section 139(9) labeling your return as "defective." You will then have a window of 15 days from the date of receiving the notice to rectify the error and file a corrected return using the right form.

Q2. Can I claim deductions if they are not mentioned in my Form 16?

Yes. If you missed submitting tax saving proofs (like health insurance or ELSS investments) to your employer, you can claim these eligible deductions directly on the income tax portal while filing your final ITR.

Q3. Is it necessary to file an ITR if my income is below the taxable limit?

While it may not be legally mandatory for everyone below the threshold, filing a "Nil ITR" is highly recommended. A clean ITR history serves as essential legal proof of income for loan approvals, visa applications, and carrying forward short-term or long-term financial losses.

Q4. What if I miss the 30-day e-verification deadline?

If you fail to E-verify your tax return within 30 days of submission, your ITR is legally treated as unfiled. This means the department will not process your return or issue any due refunds until a late condonation request is approved.

Need Professional Help with Your Tax Filing?

Don't let tax compliance overwhelm you. At Filing4U, our team of tax experts ensures your returns are completely accurate, fully optimized for maximum deductions, and submitted strictly on time.

Call us +91 7980984206

Filing your Income Tax Return (ITR) can feel like a daunting task, but it is a critical part of your financial responsibility. For Financial Year (FY) 2025-26 (Assessment Year (AY) 2026-27), the filing season comes with specific compliance updates, strict deadlines, and new tax structures that taxpayers must navigate carefully.

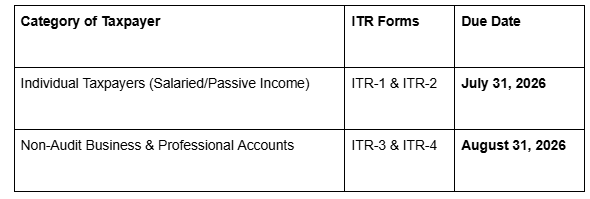

1. Choosing the Wrong ITR Form

Selecting the incorrect ITR form is one of the most frequent errors. For instance, ITR-1 (Sahaj) is meant strictly for resident salaried individuals with a total income below ₹50 lakh and no capital gains, while ITR-3 or ITR-4 (Sugam) is mandatory for individuals with income from a business or profession. Filing the wrong form can result in your return being flagged as defective under Section 139(9).

2. Quoting the Incorrect Assessment Year (AY)

For the financial year starting April 1, 2025, and ending March 31, 2026 (FY 2025-26), the correct corresponding Assessment Year is AY 2026-27. Confusing these two years is a basic error that can lead to erroneous double taxation data, delayed processing, or unnecessary penalties.

3. Errors in Personal, PAN, and Bank Information

Ensure your name, Permanent Account Number (PAN), Aadhaar number, mobile number, and email address match your official government records exactly. Additionally, if you are expecting a tax refund, double check your bank account number and IFSC code. Incorrect or unvalidated bank details are the primary reason for delayed or failed tax refunds.

4. Failing to Disclose All Income Sources

Taxpayers frequently forget to report "secondary" or passive income. You must legally disclose interest earned from savings accounts, fixed deposits (FDs), recurring deposits, rental income, and even tax-exempt income (like agricultural income or PPF interest).

Important Note: Even if a specific income source is completely exempt from tax, it must still be declared under the appropriate exempt income schedules in your return.

5. Overlooking Capital Gains Disclosure

While long-term capital gains (LTCG) on equity shares or equity-oriented mutual funds are exempt up to a specific statutory threshold (e.g., ₹1.25 lakh under updated slabs), you are still legally required to disclose these transactions. Failing to report capital gains, whether short-term or long-term will trigger an automated data mismatch notice.

6. Ignoring Form 26AS Reconciliation

Before submitting your return, you must reconcile your income and Tax Deducted at Source (TDS) with your Form 26AS. If your employer, bank, or a client has deducted tax but it does not reflect in your Form 26AS ledger, you will not receive the tax credit. This discrepancy routinely leads to a higher tax demand or a severely reduced refund.

7. Not Checking AIS and TIS

The Income Tax Department relies heavily on the Annual Information Statement (AIS) and Taxpayer Information Summary (TIS). These documents provide a comprehensive view of your high-value financial transactions, including stock market trades, mutual fund dividend distributions, and foreign remittances. Ensure the pre-filled values in your ITR match your actual bank statements and brokerage summaries.

8. Mismanaging Multiple Form 16s

If you changed jobs during the financial year, you will receive a Form 16 from both your previous and current employers. When filing, you must aggregate the salary income, allowances, and perquisites from both employers. Failing to combine this data often results in an underpayment of tax, as both employers may have independently applied basic tax exemptions.

9. Forgetting to Claim HRA Separately

If you forgot to submit your rent receipts or rent agreement to your corporate HR department before the year end payroll window closed, you can still claim the House Rent Allowance (HRA) exemption directly while filing your ITR, provided you have your landlord's PAN.

10. Missing Out on Eligible Deductions

Taxpayers frequently overlook valid deductions that can significantly lower their net taxable income. Ensure you have calculated all eligible expenditures, medical insurance premiums, educational loan interest and registered charitable donations before finalizing your submission.

11. Neglecting Advance Tax Payments

To avoid interest liabilities under Sections 234B and 234C, your estimated tax liability exceeding ₹10,000 must be paid in four installments throughout the fiscal year (June 15, September 15, December 15, and March 15). Shortfalls or delays in Advance Tax attract a 1% monthly interest penalty.

12. Misunderstanding NSC Interest Taxation

Interest earned on National Savings Certificates (NSC) is not completely tax-free. While the interest accrued can generally be reinvested and claimed as a deduction under Section 80C for the initial years, it must still be systematically reported each year under "Income from Other Sources."

13. Missing the 30-Day E-Verification Window

Filing your return online is only half the job. You must successfully e-verify your ITR within 30 days of submission via Aadhaar OTP, Net Banking, or an Electronic Verification Code (EVC). If you cannot e-verify digitally, a signed physical copy of your ITR-V must reach the Centralized Processing Cell (CPC) in Bengaluru within that strict 30-day window, or your return will be treated as invalid.

14. Failing to File Schedule AL (Assets and Liabilities)

If your total taxable income exceeds ₹50 lakh, you are mandatorily required to fill out Schedule AL. This requires a comprehensive disclosure of your physical assets (immovable properties, vehicles, bullion, etc.) along with any corresponding financial liabilities or loans.

15. Not Disclosing Foreign Assets and Income

Resident Indians must report all foreign income, foreign bank accounts and offshore assets, including global stocks, foreign mutual funds, or foreign corporate ESOPs—in Schedule FA. This is a mandatory disclosure requirement even if the income generated from these assets is not taxable within India. Non-disclosure carries severe penalties under the Black Money Act.

Important Deadlines for FY 2025-26 (AY 2026-27)

Conclusion

Avoiding these common tax filing mistakes saves you time, prevents unexpected tax demands, and keeps your financial record clean. A little preparation goes a long way toward ensuring an effortless filing season. For a completely stress-free experience, it is always recommended to compile your documents and start your filing process early to beat the last minute rush.

Frequently Asked Questions (FAQs)

Q1. What happens if I file the wrong ITR form?

If you select an incorrect form, the Income Tax Department will issue a notice under Section 139(9) labeling your return as "defective." You will then have a window of 15 days from the date of receiving the notice to rectify the error and file a corrected return using the right form.

Q2. Can I claim deductions if they are not mentioned in my Form 16?

Yes. If you missed submitting tax saving proofs (like health insurance or ELSS investments) to your employer, you can claim these eligible deductions directly on the income tax portal while filing your final ITR.

Q3. Is it necessary to file an ITR if my income is below the taxable limit?

While it may not be legally mandatory for everyone below the threshold, filing a "Nil ITR" is highly recommended. A clean ITR history serves as essential legal proof of income for loan approvals, visa applications, and carrying forward short-term or long-term financial losses.

Q4. What if I miss the 30-day e-verification deadline?

If you fail to E-verify your tax return within 30 days of submission, your ITR is legally treated as unfiled. This means the department will not process your return or issue any due refunds until a late condonation request is approved.

Need Professional Help with Your Tax Filing?

Don't let tax compliance overwhelm you. At Filing4U, our team of tax experts ensures your returns are completely accurate, fully optimized for maximum deductions, and submitted strictly on time.

Call us +91 7980984206

Copyright 2026 Filing4u. All Rights Reserved. Powered by Digital Nari

Get In Touch

Tel : +91 79809 84206

Email : info@filing4u.com

Locations : Kolkata | Bangalore | Mumbai

H.O: Industry House, 10, Camac St, Elgin, Kolkata, West Bengal 700017